U.S.-Ukraine Minerals Agreement: A Catalyst for Economic Revival

Tháng 5 1, 2025

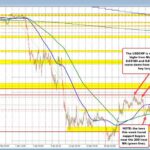

USDCHF Outlook: Balancing Between Bullish Hopes and Bearish Threats

Tháng 5 1, 2025

Understanding Tax Classifications and Holding Periods for Gold ETFs

Investing in Gold ETFs (Exchange-Traded Funds) presents a unique opportunity for diversifying portfolios and hedging against inflation. However, it is crucial for investors to navigate the various tax classifications and holding period intricacies that set Gold ETFs apart from traditional equities. These distinctions can significantly affect investment returns, especially for those unaware of the tax implications. To better understand how to maximize returns and avoid pitfalls, it may be beneficial to read about key investment mistakes to avoid in 2023 in this informative blog: Top Investment Mistakes to Avoid in 2023.

Long-Term Capital Gains (LTCG) and Gold ETFs

One of the most noteworthy aspects of investing in Gold ETFs is the classification of long-term capital gains. When Gold ETFs, such as the SPDR Gold Shares (GLD) or iShares Physical Gold ETF, are held for over 12 months, they are considered “collectibles.” This classification subjects them to a maximum tax rate of 28% for high-income earners in the United States, which is notably higher than the typical 15-20% rate applied to long-term capital gains from traditional equities.

In countries like India, Gold ETFs also face stringent capital gain tax regulations. An investment in Gold ETFs held for more than 12 months incurs a 12.5% LTCG tax. Interestingly, the capital gains tax threshold for physical gold, including gold bars and coins, is even longer, often stretching to 24 months, further complicating the comparative evaluation of these investment avenues.

Short-Term Capital Gains (STCG) and Their Implications

When Gold ETFs are sold within 12 months of acquisition, any gains realized are taxed as short-term capital gains. This taxation follows ordinary income tax rates, which can reach up to 37% in the United States. In jurisdictions like India, short-term capital gains are also subjected to individual tax brackets, thus potentially creating a financial burden for investors unaware of these implications. Investors should be mindful of common psychological pitfalls that can affect their investment decisions. This is highlighted in a blog that urges investors to maintain a balanced mindset when evaluating information: 3 Investment Mistakes to Avoid for Success.

Gold ETFs Performance and the Tax Burden

Gold ETFs have gained immense popularity, especially considering their performance metrics in recent times. With some funds, such as the UTI Gold ETF reporting a 26% return year-to-date (YTD) and the Invesco India Gold ETF at nearly 25.27%, the soaring success of these investments can lead to unexpected tax liabilities. Investors may find themselves facing significant tax burdens if they are unprepared, particularly if they believe the benefits of these ETFs outweigh the potential tax implications.

The Importance of Account Type in Tax Planning

It is essential for Gold ETF investors to recognize that the type of investment account also plays a role in tax liability. Tax-advantaged accounts, such as Individual Retirement Accounts (IRAs), can often defer or even eliminate these taxes, provided that Gold ETFs are permissible within the account structure. Utilizing these accounts can enable investors to hold onto their investments longer without immediate tax consequences.

Conclusion

As recent trends indicate that Gold ETFs have welcomed substantial inflows—evidenced by a staggering 227 tons of gold entering the global market in the first quarter of 2025—it’s imperative for investors to understand the varied tax classifications and holding periods associated with these financial instruments. By equipping themselves with knowledge and leveraging appropriate investment accounts, investors can navigate the complexities of Gold ETF taxation, enhancing their overall investment strategy while minimizing potential liabilities.