US Import Prices and NY Fed Manufacturing Index Fuel USD Volatility

Tháng 4 16, 2025

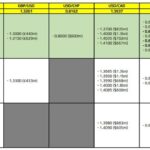

Decoding FX Option Expiries: Navigating Market Sentiment Ahead of April 2025

Tháng 4 16, 2025Understanding the NY Fed Manufacturing Index Surge

Implications of the NY Fed Manufacturing Index at -8.1

A recent report highlighted the NY Fed Manufacturing Index registering at -8.1, a significant contraction that sparked widespread concern across financial markets and among economic analysts. This negative reading suggests that a substantial segment of manufacturers in the New York region is confronting challenges, including decreased orders, rising costs, and supply chain disruptions. Such a drop below the neutral mark of zero indicates that business conditions are deteriorating, which could have broader implications for economic growth and employment.

The implications of this contraction are profound, revealing potential weaknesses in the manufacturing sector that could influence overall economic momentum. A reading of -8.1 reflects not only a reduction in current manufacturing activity but also suggests a lack of confidence among businesses regarding future economic conditions. This sentiment could lead to reduced capital investments, hiring freezes, or layoffs, thereby impacting job creation in an already fragile labor market.

Moreover, the adverse conditions reflected in the NY Fed index might prompt policymakers to reconsider monetary and fiscal strategies. The Federal Reserve, for instance, may alter its approach towards interest rates if such weaknesses persist, potentially leading to more accommodative policies aimed at stimulating growth. Thus, the -8.1 reading serves as a critical signal for stakeholders to monitor, as it foreshadows potential shifts in economic policy and market dynamics.

Comparison with Forecasts and Previous Data

An analysis of the NY Fed Manufacturing Index at -8.1 also necessitates a comparison with both forecasts and previous data to understand its context better. Forecasts leading up to the release typically anticipated a more modest reading, perhaps around zero or slightly positive. For example, many economists predicted the index would hover around 1.0 to 2.0, reflecting expectations of stability in the manufacturing sector.

This stark contrast underscores the element of surprise and adds weight to the concerns surrounding economic health. When actual performance deviates significantly from these forecasts, it tends to amplify market reactions. The index falling to -8.1 not only shocked analysts but also elicited immediate reactions in financial markets, as investors adjusted their expectations for corporate earnings and overall economic growth in the upcoming quarters.

When comparing this current figure to prior months, the deterioration is even more pronounced. Previous readings may have shown stability or even mild expansion; for instance, if the index were at 5.0 just a few months ago, the current result indicates a rapid decline in sentiment. Such comparisons highlight the increasing severity of challenges facing manufacturers and signal a potential slowdown in economic recovery efforts that had previously shown promise.

In summary, understanding the implications of the NY Fed Manufacturing Index at -8.1 involves examining its significance for both current economic conditions and future expectations. The index’s comparison with forecasts and previous data provides essential context, reflecting sharp shifts in manufacturing sentiment that could prompt policymakers to act. Stakeholders must carefully monitor these developments as they navigate the evolving economic landscape, using insight gleaned from the index to inform their strategies and decision-making processes.

Analyzing US Import Prices and Export Prices

Decline in Import Prices: A Closer Look

The recent decline in U.S. import prices has become a focal point for economists and market analysts, prompting further investigation into the factors driving this trend and its broader implications for the U.S. economy. Recent data has indicated a notable decrease in import prices—around -0.4%—which can be attributed to various elements, including reductions in transportation costs, favorable exchange rates, and improving supply chain conditions.

This decline is significant as it suggests increased purchasing power for American consumers and businesses. Lower import prices can lead to decreased costs for essential goods such as electronics, textiles, and food. For consumers, this can mean more affordability, potentially stimulating consumer spending, which is vital for economic growth. Additionally, businesses that rely on imported materials for production can benefit from lower costs, enhancing profit margins that may otherwise have been pressured by inflation.

However, it is essential to view the decline in import prices within a broader economic context. If the decrease signifies diminished demand due to slower economic activity or consumer confidence, it could indicate underlying economic weaknesses. This worrying trend might lead to reduced investment by companies anticipating lower future sales, ultimately affecting job creation and economic growth.

Furthermore, as import prices fall, there could be implications for U.S. trade balances and competitiveness. While lower import prices can alleviate inflationary pressures, they may also result in a widening trade deficit if import volumes exceed export values and demand for U.S. goods does not keep pace. Therefore, while the decline in import prices brings certain benefits, it is critical to remain vigilant about the potential risks it poses to economic stability.

Impact of Export Prices Stagnation

While import prices have declined, the stagnation of export prices presents another layer of complexity in understanding the U.S. economic landscape. When export prices stabilize or show little movement, it raises critical questions about the competitiveness of U.S. goods in the global market. If U.S. manufacturers are unable to command higher prices for their exports, it could signal challenges in maintaining market share against international competitors.

The stagnation of export prices can have far-reaching implications for the U.S. economy. For one, it can adversely affect the profit margins of manufacturers, limiting their ability to reinvest in operations or expand their workforce. If companies struggle to maintain sales abroad due to stagnant pricing levels, they may face difficult decisions regarding layoffs or production cuts, which could underline deeper economic fragility.

Moreover, a lack of growth in export prices can impact the overall trade balance. When the value of exported goods does not rise at a healthy rate, and import prices decrease simultaneously, it can lead to a widening trade deficit. This situation raises concerns among policymakers regarding domestic competitiveness and the long-term sustainability of the U.S. manufacturing sector.

Additionally, if stagnation persists, it could hinder economic recovery efforts. A robust export market is crucial for driving economic growth; thus, stagnating prices may reflect broader issues within the global economy or shifts in consumer preferences that U.S. manufacturers need to navigate.

In summary, analyzing U.S. import and export prices reveals vital insights into the current state and future trajectory of the economy. While the decline in import prices presents immediate benefits for consumers and businesses, the stagnation of export prices underscores potential challenges facing U.S. manufacturers and highlights the interconnectedness of domestic and global economic dynamics. Stakeholders must remain attentive to these trends, as their implications will significantly shape future economic conditions and policy responses.

Effects on USD Volatility and Market Reactions

Market Volatility Following Economic Releases

Market volatility often spikes in response to key economic releases, reflecting how sensitive currency traders are to new data that can influence economic forecasts and monetary policy. Each month, important reports—such as employment figures, inflation data, and manufacturing indices—are closely watched by traders, as they provide insights into the health of the U.S. economy. When these figures deviate significantly from expectations, the currency markets can react sharply, leading to rapid fluctuations in USD value.

For example, if a report indicates unexpectedly strong job growth, the dollar may experience a significant rally as traders anticipate a potential interest rate hike from the Federal Reserve. Such positive economic data increases confidence in the dollar, prompting buying pressure. Conversely, if economic data falls short of expectations, it can lead to heightened volatility as traders rush to recalibrate their positions. The dollar may depreciate against other major currencies, reflecting concerns about economic slowdown and reduced monetary tightening.

This immediate reaction to economic releases can create an environment where volatility becomes a norm. Traders must stay agile, as positions may need to be adjusted in the wake of new information. Additionally, around the release of critical data, market participants often experience heightened anxiety, leading to increased trading volumes and sometimes overshooting moves—where the dollar swings more dramatically than the economic news might justify.

The interplay between economic releases and market volatility emphasizes the importance of sentiment in the currency market. Traders may overreact or underreact based on their perceptions of economic conditions, which can lead to temporary distortions in USD value. Understanding these dynamics allows currency traders to navigate their positions more effectively.

USD Performance in the Currency Market

The performance of the U.S. dollar in the currency market is intricately tied to the reactions stemming from economic data. As an important global currency, the USD’s strength or weakness influences not only domestic markets but also global economic conditions. When the dollar appreciates, it often reflects confidence in U.S. economic growth, leading to foreign investment inflows and bolstering its status as a safe-haven currency.

Following significant economic releases, we often observe pronounced movements in the USD against other key currencies, such as the euro, Japanese yen (JPY), and British pound (GBP). For instance, if U.S. manufacturing data significantly exceeds forecasts, the USD typically strengthens against these currencies. Traders may interpret such performance as an indication of a robust economic recovery, which can lead to a reassessment of investment strategies.

On the other hand, if economic indicators suggest weaknesses—such as declining consumer confidence or rising unemployment—the dollar may weaken as market participants flock to alternative currencies or safe-haven assets like gold. The USD’s performance is not only driven by U.S. economic conditions but also by the relative health of other economies. If the eurozone or Japan shows resilience amid U.S. economic struggles, it can further impact USD valuations, shaping trading strategies in the currency market.

In summary, the effects on USD volatility and market reactions highlight the critical relationship between economic data releases and the value of the dollar. Market participants must remain vigilant, as shifts in sentiment and expectations can lead to rapid changes in currency valuations. The dynamic nature of the currency market requires traders to continually assess economic conditions and their implications for USD performance, positioning themselves to seize opportunities in this ever-evolving landscape. Understanding these trends is essential for making informed trading decisions and effectively managing risks in currency markets.

Implications for Economic Resilience and Inflation

Market Expectations on US Economic Resilience

The concept of economic resilience encapsulates the ability of an economy to withstand or recover from various shocks while maintaining stable growth. Recent trends in U.S. economic indicators have led market participants to closely analyze the underlying factors contributing to perceptions of resilience in the economy. As key data releases reflect ongoing strength in certain sectors—such as manufacturing and consumer spending—investors remain optimistic about the potential for sustained growth, despite challenges such as rising interest rates and geopolitical uncertainties.

Market expectations regarding U.S. economic resilience are heavily influenced by factors such as employment rates, consumer confidence, and business investment. A strong labor market, characterized by low unemployment and rising wage growth, tends to bolster consumer confidence, leading to increased spending. This cycle of growth reinforces perceptions of resilience and encourages investors to remain engaged in U.S. markets. Conversely, any signs of weakness—such as declining manufacturing output or deteriorating consumer sentiment—can spark concerns about weak economic performance, leading to volatility in asset prices, including the U.S. dollar.

Moreover, market expectations reflect the intricate interplay between economic conditions and monetary policy. The Federal Reserve’s decisions on interest rates and inflation targeting can shape perceptions of resilience significantly. For instance, if the Fed indicates a commitment to combating inflation while maintaining economic growth, it may bolster confidence in the economy’s ability to adapt to changing conditions. As a result, the USD may appreciate as global investors seek to capitalize on perceived stability and momentum in the U.S. economy.

Inflation Trends and Their Influence on USD Valuation

Inflation trends are central to understanding the implications for USD valuation and overall economic health. As inflation rises, it can erode purchasing power, leading to increased costs for consumers and businesses. Recent inflationary pressures, driven by various factors such as supply chain disruptions and rising energy costs, have captured the attention of policymakers and market participants alike.

When inflation trends upward, the Federal Reserve is often compelled to act by tightening monetary policy through interest rate hikes. Investors closely monitor these developments, as rising interest rates generally lead to currency appreciation because higher rates attract foreign capital seeking improved returns. Therefore, if inflation continues to rise, the expectation of aggressive rate hikes can strengthen the USD.

Conversely, persistent inflation without corresponding increases in interest rates may raise concerns about the Fed’s ability to manage economic stability. In such cases, the market might react with skepticism regarding the dollar’s long-term value as consumers and businesses adjust to increasing prices. If expectations shift towards potential economic stagnation accompanying high inflation—often referred to as stagflation—the dollar could face depreciation due to weakened confidence in the U.S. economy.

In summary, the implications for economic resilience and inflation are intertwined with perceptions of the U.S. economy’s strength and market expectations. As evidence of resilience emerges, fueled by robust economic indicators, market participants may continue to support the dollar. However, navigating the delicate balance between inflation management and economic growth will be critical for policymakers. Understanding these dynamics will help stakeholders position themselves effectively in the ever-changing landscape of currency valuation and economic performance. The interplay of resilience and inflation remains a central focus in evaluating the future trajectory of the U.S. dollar and the broader economy.

Global Currency Market Reactions

The Stability of the JPY Amid USD Fluctuations

In the ever-evolving realm of the global currency market, the Japanese yen (JPY) has shown a remarkable ability to maintain stability amid the recent fluctuations of the U.S. dollar (USD). Traditionally regarded as a safe-haven currency, the yen tends to attract investors seeking refuge during times of uncertainty or market volatility. As economic conditions fluctuate, characterized by changing economic indicators and geopolitical developments, the JPY’s ability to hold its ground against the dollar illustrates its resilience and the confidence that investors place in the Japanese economy.

For instance, during periods of heightened uncertainty, such as sharp declines in U.S. stock markets or disappointing economic data, the yen often appreciates against the dollar as traders seek safer assets. This trend can be observed when data releases from the U.S. suggest potential weakness, prompting market participants to shift their focus toward currencies that promise more stability. Additionally, the Japanese economy’s relatively robust fundamentals, including low debt levels and a strong trade surplus, contribute to the yen’s stability in the face of USD fluctuations.

However, the stability of the yen is also influenced by Japan’s own economic conditions, including interest rates and inflation. The Bank of Japan (BoJ)’s ongoing commitment to accommodative monetary policy has kept interest rates at historically low levels, which limits the yen’s potential for significant appreciation. Nonetheless, the interplay between global economic conditions and domestic policy remains crucial in maintaining the yen’s stability as market dynamics continue to shift.

Broader Impacts of Mixed Data on Currency Pairings

The currency market’s landscape is often shaped by a mosaic of economic data from various countries, leading to mixed outcomes in currency pairings. When economic indicators release conflicting signals—such as stronger-than-expected employment data in the U.S. coupled with declining manufacturing numbers—the resultant market reactions can create widespread volatility across various currency pairs.

In such scenarios, currencies tied to economies showing resilience may experience enhanced performance compared to those facing headwinds. For example, if the eurozone releases positive GDP growth figures while U.S. manufacturing data flounders, the EUR/USD pairing might strengthen significantly as traders respond to optimistic expectations surrounding the euro. Conversely, if market participants perceive that the associated data from the U.S. hints at a potential economic slowdown, the dollar could weaken against not just the euro, but also other currencies like the British pound (GBP) and Swiss franc (CHF), leading to a ripple effect on trading strategies.

Additionally, mixed data often influences traders’ risk appetite, prompting them to engage in carry trades or swing trading strategies that capitalize on discrepancies between interest rate expectations in different economies. For instance, if U.S. data suggests a slowing economy while the Reserve Bank of Australia (RBA) signals a more hawkish stance, traders might favor the Australian dollar (AUD) over the USD, shifting positions accordingly.

The reactions to mixed data not only reflect immediate trading strategies but also highlight global investor sentiment and risk perceptions. As trends develop, markets can become particularly volatile, leading to rapid movements in currency pairings throughout trading sessions. Investors and analysts must remain vigilant, continuously reassessing their strategies based on the economic landscape and the currency dynamics that emerge in response to forthcoming data releases.

In summary, the global currency market reactions reveal the intricate and interdependent nature of currency pairings amid fluctuating economic indicators. The stability of the JPY in the context of USD fluctuations underscores the dynamics of safe-haven currencies, while the broader impacts of mixed data on currency pairings illustrate the complex relationships that define trading in the currency market. Understanding these nuances is critical for navigating the always-changing landscape of global finance and currency valuation.